VN stock market ready for rebound as negative factors abate: VinaCapital

All transient negative factors have already abated or are easing, and the prospects for higher Vietnamese stock prices in the months ahead are supported by rebounding earnings growth, a rebounding economy, and the market’s cheap valuation, according to VinaCapital.

The negative factors that affected the stock market are in the rear-view mirror or getting there, and the prospects of higher stock prices in the months ahead are supported by rebounding earnings growth, a recovering economy and cheap valuations, according to Michael Kokalari, chief economist at VinaCapital.

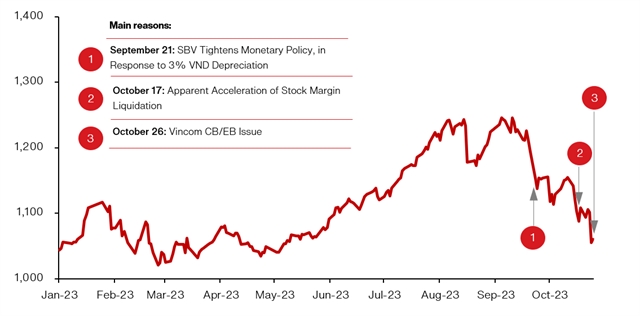

In his latest report, he said the VN-Index saw a 16 per cent sell-off between mid-September and end-October despite the fact that the economy is now recovering from its earlier slowdown.

He mentioned three key factors driving the sell-off.

The depreciation of the đồng prompted concerns that the State Bank of Vietnam would significantly tighten monetary policy and prompted some selling by foreign investors, he said.

The announcement of Vingroup’s US$250 million convertible bond, exchangeable into Vinhomes shares, caused its share price to drop by more than 10 per cent, he said.

That drop in turn weighed on investors’ sentiment towards VIC somewhat -- VIC and VHM account for about 10 per cent of the VN-Index -- and this was the second factor, he said.

Thirdly, margin calls by local securities companies and rumours of a clampdown on certain unofficial sources of margin lending appeared to have prompted an unwinding of highly leveraged speculative positions on October 17, he said.

Besides, the 60-basis-point increase in 10-year US Treasury yields from mid-September to end-October and geopolitical issues also weighed on emerging market stock markets, with the MSCI-EM Index falling 5 per cent in that period, he pointed out.

But the VN-Index significantly underperformed its regional emerging market peers, making it clear that concerns about the SBV and VIC/VHM drove the sell-off, he explained.

Q3 earnings have generally been lacklustre, which also weighed on investor sentiment to some extent, he said.

“We expect EPS earnings growth to rebound to 35 per cent y-o-y in Q4 2023 and 20 per cent in 2024 largely because the sharp slowdown in Việt Nam’s economy earlier this year has clearly ended, evidenced by a rebound in GDP growth from 3.3 per cent y-o-y in Q1 to 4.1 per cent in Q2 and 5.3 per cent in Q3.

“The main factor weighing on Việt Nam’s economy had been a slowdown in exports to the US, but high-frequency economic data for October confirmed our recent assertions that VIệt Nam’s manufacturing activity and exports are now recovering, reinforcing our expectation that GDP growth will rebound to 6.5 per cent next year.”

Despite those clear signs of economic recovery, valuation of the VN-Index on both forward P/E and P/B bases fell to a level seen only twice in the past 10 years, he said.

Furthermore, trading volumes more than halved from $1.3 billion a day before the sell-off to $500 million in late October.

Stock market technicians characterise reduced selling enthusiasm during a sharp market decline as a likely sign that the market will enjoy a robust rebound once the factors causing the sell-off abate, which helps explain the fairly strong performance of the market by the end of the first week of November.

“From our point of view, all of these transient negative factors have already abated or are easing, and the prospects for higher Vietnamese stock prices in the months ahead are supported by rebounding earnings growth, a rebounding economy, and the market’s cheap valuation,” Kokalari said. — VNS