Stock market to benefit from unexpectedly strong domestic growth: VinaCapital

July economic statistics have not only reinforced VinaCapital’s forecast of 7.5 per cent GDP growth in 2022 but also make it look like the economy would grow by a stunning 10 per cent year-on-year in the current quarter.

“Viet Nam’s economy is even stronger than we had expected at the beginning of the year, but that strength is not reflected by higher stock prices due to the [US’s] aggressive rate hikes and the recent regulatory crackdown in Viet Nam,” Michael Kokalari, chief economist at VinaCapital, has said in a report.

“That said, we expect over 20 per cent [company earnings] growth in 2022, which should support a recovery in the VN-Index by the end of 2022.”

July economic statistics have not only reinforced VinaCapital’s forecast of 7.5 per cent GDP growth in 2022 but also make it look like the economy would grow by a stunning 10 per cent year-on-year in the current quarter, he said.

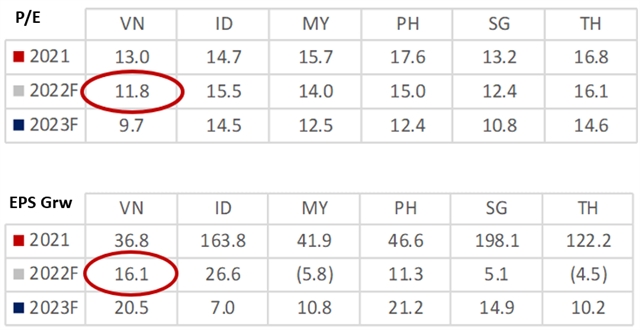

“Our expectation that Viet Nam’s economy will grow by at least 7.5 per cent this year (and by at least 10 per cent in Q3) leads us to believe that the consensus forecast for 16 per cent [company] earnings growth this year in Viet Nam is too conservative.

“We expect earnings growth to exceed 20 per cent this year, supported by Viet Nam’s solid economic performance – in stark contrast to the US stock market, where earnings growth expectations look unrealistically high, especially given that country’s deteriorating economic outlook.”

Viet Nam’s retail sales have accelerated all year, illustrating that consumption is currently the main growth driver, he said.

In the first half of the year retail sales adjusted for inflation grew by 7.9 per cent, and surged to 11.9 per cent in the first seven months, far above the 7 per cent growth his company had previously forecast, he said.

“This is important because we are often asked now whether the ongoing slowdown in the US economy, Viet Nam’s biggest export market, will weigh on Viet Nam’s economic growth.”

A slowing US economy is likely to temper Viet Nam’s export growth and economic growth, but that would be more than offset by Viet Nam’s strong domestic economy, he said.

“The revenues and earnings of companies listed on Viet Nam’s stock market are primarily driven by the domestic economy, which is why we would have expected the stock market to benefit from the unexpectedly strong domestic growth.”

The stock market rose 37 per cent in 2021, driven by a 36 per cent rise in earnings.

“All of this makes it somewhat surprising that the VN-Index is currently down 17 per cent year-to-date.”

The main reason for the recent dour sentiment among retail investors is the Government’s regulatory crackdown on illegal practices by certain companies that started at the end of March, he said.

“But we believe the Government’s efforts to improve corporate governance and transparency in Viet Nam will ultimately benefit the stock market and the country as a whole.”

The issue has had less impact on the stock market in recent weeks, and Viet Nam already has the highest transparency and political stability ranking in Southeast Asia, according to a report from the Political & Economic Risk Consultancy, he said.

Coming Bounce in the VN-Index

VinaCapital expects another leg down in the US stock market, which could in turn drag Viet Nam’s stock market lower.

Kokalari said: “However, at some point we expect the Fed to ‘pivot’ away from its aggressive rate hike plans. Viet Nam’s stock market should be one of the biggest beneficiaries of a Fed pivot because Viet Nam has the most attractive valuation in the region, and the second highest expected earnings growth next to Indonesia.

“Furthermore, the quality/visibility of Viet Nam’s corporate earnings is currently much better than that of Indonesia and other regional peers.”

He also expects bank share prices to outperform in the second half of the year, as it becomes apparent that banks’ post-COVID asset quality issues are much less severe than many investors had feared, especially in light of Viet Nam’s very high GDP growth in 2022. — VNS